Let’s look at the just-announced Jan-Oct CIPA numbers for the past few years for a moment:

DSLRs fell to half their previous sales level in just four years. Mirrorless is running 11% under its peak. Since Canon and Nikon essentially own the DSLR market they’re under extreme stress; particularly Nikon, where a majority of their business is cameras.

But another way of looking at the CIPA numbers is more illustrative:

- 2012 — 1.945 trillion yen

- 2013 — 1.672t

- 2014 — 1.431t

- 2015 — 1.335t

- 2016 — 1.080t (generous estimate)

This is the cumulative total value of all compacts, mirrorless, DSLRs, and lenses shipped by Japan. When I write “generous estimate,” I’m using the previous year's November and December sales as predictions to be added to the actual January through October for 2016. Still, a drop of 44%.

To put that in context, The US gross domestic product from 1929 to 1933 (the Great Depression) dropped 45%. Ouch.

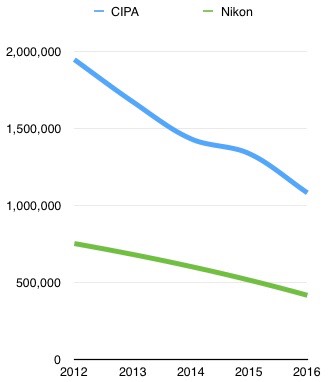

Nikon’s fiscal year is a quarter off from the calendar year CIPA uses, but here are those same numbers for the Nikon Imaging group (all cameras/lenses) for the similar period:

- 2012 — 751 billion yen

- 2013 — 684b

- 2014 — 586b

- 2015 — 520b

- 2016 — 415b (Nikon forecast)

Again, those are offset by one quarter (e.g. 2016 extends one quarter into 2017). Moreover, CIPA doesn’t track accessories, which would be in Nikon’s numbers. Still, here’s what those look like graphed together:

The word I get out of Tokyo is mixed. About half those I communicate with seem to think that 2016 would have represented a flat year to 2015 if it hadn’t been for the quake. The other half say that the quake just revealed reality.

They’re probably both right. Had the quake not shut off sensor supply, I’m pretty sure the Japanese camera companies would have tried to ship far more units and at higher value than the estimate says they will. Anything above 1.2t yen would be considered a “flattening” of the market decline. Anything above 1.3t yen would be considered “we hit bottom.”

But if you look at the retail sales numbers here in the US (cash register receipts from one of the companies that collect this, such as NPD), you see that camera sales are weak even with the restricted supply due to the quake, and remember that the US is a strong economy compared to other places you might want to sell cameras. (I’m told by someone who’s seen similar numbers out of Europe that he sees the same thing there: very poor demand and sell through.) The units that arrived here in the US in 2016 so far just aren’t jumping off the shelves. Had more inventory been shipped, it’s almost certain that it would have required instant rebates and sales to move those units.

So as we get to the close of another year, I’d have to argue that “nope, we haven’t hit bottom yet.”

That’s where things get really scary. If this is just a constant state of decline, DSLRs will fall below 3m units by 2021, which is about where mirrorless is now.

The question is this: what breaks the on-going decline? Nothing so far. Nothing currently foreseeable.