(news & commentary)

We can pretty much expect Nikon to report continued profits for the past quarter next month (Canon already did), and the rest of the camera companies may be reporting slightly better news than expected, too. Why? Simple: they stuffed the channel in March. Okay, they may have also reduced their costs slightly, too.

The CIPA numbers indicate increased shipments in March pretty much across the board, even in compact cameras. Retail sales numbers show drops in most categories. The production numbers tell a slightly different story, too, with compacts significantly down and only 54% of last year’s March numbers.

Coupled with an average selling price increase also almost across the board, it appears that the Japanese companies were trying to get their quarterly numbers up as high as possible to disguise the more troubling trends.

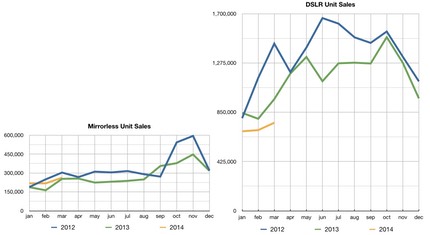

First, the current graphs:

2014 Q1 for mirrorless was 116% compared to last year, but for DSLRs it was 82%. Canon and Nikon seemed to have put just enough product into the channel to keep their numbers showing only slight drops once the average selling price is figured in. As for the mirrorless gains, remember that mirrorless is highly popular in Japan. Unfortunately, starting this month the sales tax increased in Japan, making buying a camera there more expensive, and everyone was pushing product last quarter in anticipation of lower sales in the future (see Canon results, below). The US still seems to be the exception when it comes to mirrorless, with shipments down to less than 20k units in March and only 58% year-to-year. But even our appetite for DSLRs is waning year-to-year, too, while DSLR shipments to Asia were double what they were to the US in March (which could just be selling into the gray market, not actual sales to Asian customers).

This is the point in the year where I do my yearly forecast of units:

- Compacts: 28-30m units (CIPA forecast is 33.8m)

- Mirrorless: 2.8-3m units

- DSLRs: 10m units (CIPA forecast for Mirrorless+DSLR is 14.2m units)

My forecasts are based on the assumption that the Japanese companies are also able to reduce the dealer inventories of older generation products significantly. At the current or higher selling prices, the channel won’t stand any more stuffing. Of course, if someone has a breakthrough product in the wings that can really rekindle buying excitement, all forecasts will be off. But even though this is a Photokina year, Photokina products have a tendency to slip into the following year in terms of significant shipments.

I mentioned a troubling trend earlier. Compacts are way down. But look at the DSLRs: they' are down for the third consecutive year. Indeed, we’ve had 13 consecutive months where DSLR sales have declined year-to-year. Meanwhile, mirrorless sales are bouncing around a bit, with 4 of the last 13 months being up year-to-year, 9 being down, though 3 of those 4 happened in the last quarter. There simply isn’t any meaningful growth showing anywhere in the market. If mirrorless is the new “Golden Goose,” no one is going to get rich off it, as the implied “growth" is less than 100k units overall (and remember, I believe the channel was stuffed, too). Indeed, historically what happens is that the companies all scramble to where the least worst problems are. That would be mirrorless right now, so it’ll just be more players fighting over the scraps.

Canon was the first to report first quarter results, as usual. I like the way they worded things: “sales…of interchangeable-lens digital cameras declined owing to the priority placed on optimizing inventories in the market.” In other words, the channel is already stuffed, so they couldn’t stuff more in. SG&A expenses remained constant at around 31%, a slightly high number, but not increasing as it is in other camera companies with channel inventory issues. That’s a good sign.

That said, Imaging sales were off by about 2% year-to-year for Canon, while the rest of their businesses showed double-digit gains. I should also note that the Imaging group includes inkjet printers, and Canon specifically noted that consumables for them had healthy growth. Indeed, the inkjet printer sales grew from 26% to 29% of the group’s sales, while cameras declined from 65% to 62%. That makes digital cameras about 21% of Canon’s total sales.

Imaging group profit rose significantly over last year, but that’s more of an indication that Canon has absorbed the initial shock of the digital camera decline and adjusted its offerings to emphasize higher end gear. Operating costs in the Imaging group were significantly down year-to-year, also indicating better cost controls. Put another way, Canon has successfully tightened their belt in the Imaging group.

Still, there are some eyebrow raising numbers in their disclosures. Imaging sales to Japan for the quarter were up 33%, but the Americas down 17.1%. This probably was the pre-sales tax increase push in Japan, but the Americas are 22% of their sales and have a healthy economy at the moment, while Japan ballooned from 13% to 18% of their sales in a doldrum economy. That looks like channel stuffing to me. Also telling was the Forex (foreign currency exchange) number: the change in the value of the yen had a bigger impact on sales than did changes in their sales volume. Sales were up 51.6b yen, but 56.5b yen of that was due to Forex! That Canon is predicting flat currency for the rest of the year is a potential warning signal on lack of sales growth (see page 9 of their Presentation Material).

Interchangeable lens camera sales were down 7% year-to-year, with compacts down 30%. 41% of Canon’s camera sales are now interchangeable lens cameras and lenses. Canon reduced their interchangeable lens camera estimates for the year slightly, though they’re still unbelievably high compared to what’s happened so far this year and the CIPA estimates for the year. So much so that it implies taking significant market share from Nikon.

Here’s my guess: Nikon will be targeting mostly high for the rest of this year in interchangeable lens cameras: D7300, D9300, D800s and/or D4x. You can make up some of the sales problem by selling fewer higher priced units. But eventually you have to face reality: with unit volume dropping in Coolpix, no real growth in Nikon 1, and falling sales in consumer DSLRs, this implies contraction for the near term. If Nikon does produce the D300 and D800 followups, those are “not going to buy another camera anytime soon” types of purchases (though they may increase lens purchases).

One other point: while the Internet has managed to put a lot of hype on a lot of products over the past year, overall sales aren’t going the direction the hype is. I have this feeling that the hype will ratchet up even higher this year while the sales continue to be rather mediocre at best. I’d love to be proved wrong and see camera sales take off again, but it just doesn’t seem to be in the cards. 20k units a month of an individual product is starting to look like a big hit these days.